A year rich in events has passed for the UK gambling industry only to march into a new one that may prove to be even more challenging. A crackdown on the fixed-odds betting terminals is looming. Regulatory measures are expected to be introduced, ones that will probably change the UK gambling landscape in a manner that will be found particularly unfavourable to operators with long heritage in the retail gambling trade.

A year rich in events has passed for the UK gambling industry only to march into a new one that may prove to be even more challenging. A crackdown on the fixed-odds betting terminals is looming. Regulatory measures are expected to be introduced, ones that will probably change the UK gambling landscape in a manner that will be found particularly unfavourable to operators with long heritage in the retail gambling trade.

Yet, if growing concerns are set to the side for a moment, it should be noted that UK gambling has grown into a prosperous industry over the past decade. It could be said that its evolution into one of Europe’s (and probably the world’s) largest markets has started centuries ago. After all, the UK is the birthplace of some of the oldest and largest bookmakers. However, particular changes in the country’s gambling regulations, ones that aimed to modernise, set a regulatory framework with clearer-cut definitions, and regulate formally sectors that have not been regulated before, were introduced in 2005 and enhanced the industry’s growth in a sufficiently important manner.

Devised to relax certain restrictions and to strengthen others, the Gambling Act 2005 turned out to be a formative piece of legislation with a profound influence on the nation’s gambling industry.

Gambling Act 2005 and How It Changed the Industry

The Act was designed to exercise control over the way gambling products and services were provided to UK-based customers. Its contents included provisions for the regulation of all types of gambling facilities and offering available within the UK borders as well as for the promotion of responsible gambling so as for customers to be able to gamble in as safe and well-controlled environment as possible. Dwelling in detail on the whole Act would be of little relevance to the main purpose of this article.

However, it is important to note that two particularly significant changes in the UK gambling industry were brought by that piece of legislation. In the first place, the UK Gambling Commission was formed as required by the Act. The regulatory body replaced the Gaming Board for Great Britain in overseeing the local industry.

The Gambling Commission came into being on 1 October 2005. Three key objectives were put before the regulator upon its formation – to oversee the industry, working closely with the Government and other concerned parties; to keep gambling crime-free and to make sure that services are provided in a fair and open manner; and to protect the most vulnerable members of population from falling victims to excessive gambling and gambling addiction. Of course, these three objectives have branched out into multiple sub-tasks over the years and as the industry has grown.

At present, the Gambling Commission regulates arcades featuring gambling machines, betting operations, both land-based and online, bingo halls across the nation and bingo websites, brick-and-mortar and online casinos, and lotteries, including the National Lottery.

In the second place, the Gambling Act 2005 regulated UK’s remote gambling market, providing sharply defined provisions of how remote gambling operations should be conducted in the country. Bearing in mind how quickly digitalisation came upon us and entered every (or almost every) aspect of our lives, it could be said that the Act implemented necessary changes in that direction, changes that eventually placed UK among the jurisdictions with the most highly lucrative and most rapidly growing markets, particularly when it came to online gambling.

Gambling (Licensing and Advertising) Act 2014 – Another Change of Course

The Gambling (Licensing and Advertising) Act 2014 received Royal Assent on 14 May 2014 and came into effect on 1 November 2014. It required all remote gambling operators providing products to British customers to obtain a license from the Gambling Commission. In other words, the Act regulated the industry based on the point of consumption.

Prior to that, remote gambling operations had been regulated at the point of supply. To be more precise, operators whose gambling facilities had been available to British customers but their equipment had not been located in the UK had had no need of Gambling Commission-issued license. If, however, their equipment had been based within UK’s borders, they had been required such a license.

UK Gambling Industry General Overview

The period between 2005 and 2007 was a transitional one for the UK gambling industry. This two-year period encompassed events related to the introduction of the Gambling Act, its adoption, and the gradual implementation of all its provisions. To be more precise, it was not before September 2007 that the law came fully into effect.

Among its many tasks, the Gambling Commission was also responsible for monitoring the industry’s financial performance; whether it has been growing or contracting over the years. Following the regulator’s establishment and the complete adoption of the Gambling Act 2005, the body compiled and published its first comprehensive industry financial report for the period April 2008-March 2009. From that point on, the Gambling Commission has been preparing and publishing such reports every year.

| UK Gambling Industry by Sector (GGY £ million) | ||||||||

|---|---|---|---|---|---|---|---|---|

| April 2008-March 2009 | April 2009-March 2010 | April 2010-March 2011 | April 2011-March 2012 | April 2012-March 2013 | April 2013-March 2014 | April 2014-March 2015 | April 2015-March 2016 | |

| Arcades | 480.35 | 455.96 | 392.00 | 381.06 | 358.71 | 379.15 | 379.83 | 382.67 |

| Betting | 2,903.24 | 2,811.36 | 2,957.32 | 3,029.59 | 3,198.60 | 3,174.84 | 3,269.59 | 3,306.21 |

| Bingo | 703.11 | 627.22 | 625.58 | 680.64 | 700.90 | 671.29 | 663.45 | 687.04 |

| Casinos | 796.17 | 751.13 | 797.43 | 872.80 | 961.41 | 1,111.06 | 1,159.54 | 998.08 |

| Remote Gambling | 816.86 | 632.22 | 653.06 | 710.19 | 932.61 | 1,134.66 | 2,238.82 | 4,468.64 |

| National Lottery | 2,521.50 | 2,679.20 | 2.840.20 | 3,123.90 | 3,279.50 | 3,099.80 | 3,232.10 | 3,416.80 |

| Other Lotteries | 143.69 | 158.55 | 170.12 | 228.61 | 273.00 | 293.79 | 344.78 | 371.55 |

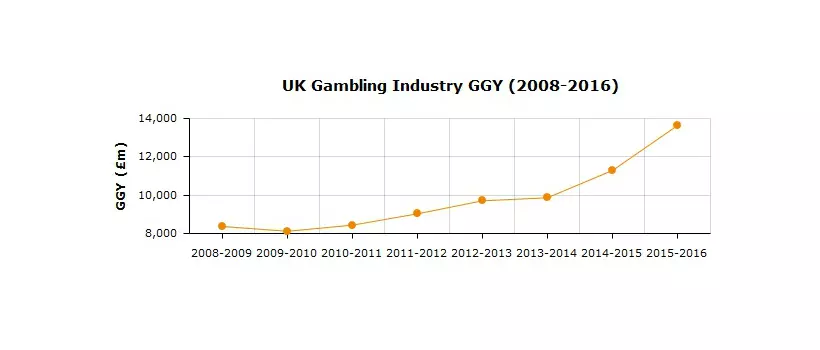

| Total | 8,364.92 | 8,115.64 | 8,435.70 | 9,026.80 | 9,704.74 | 9,864.60 | 11,288.11 | 13,631.00 |

Table 1: Gambling Industry GGY (£m) 2008-2016

Table 1 shows several important trends that need to be paid a bit more special attention. Here it is important to note that it includes information about the gross gambling yield (GGY) generated by all gambling operations, both land-based and remote, provided within the UK’s borders. In general, GGY is the amount kept by gambling operators after winnings are paid out but before operation costs are deducted.

It could be seen from the table above and from the chart below that the UK gambling industry has been growing constantly since April 2008. The period April 2009-March 2010 represented the only exception to the overall upward trend. The amount of £8.1 billion was generated during the reviewed twelve months, down from £8.4 billion reported for the same twelve months a year earlier. Results improved during the very next year, as it can be seen.

The period between April 2015-March 2016 was the most profitable one for the UK gambling industry. The Gambling Commission reported a total of £13.6 billion for said twelve months, up significantly from the amount of £11.3 billion generated during the prior-year period. As revealed by the country’s gambling regulator, the considerable growth could, to a great extent, be attributed to the accelerated GGY rise in the online segment.

Looking at the period between April 2008 and March 2015, high street betting was UK’s largest gambling sector for the greater part, rivalled only by the National Lottery. Betting reached its highest of £3.3 billion in the twelve months between April 2015 and March 2016. However, during that period, it was dethroned by remote gambling as the most profitable gambling sector. Remote gambling operators generated a total of £4.5 billion during the reviewed twelve months, reflecting an increase from £2.2 billion generated in the prior-year period.

The UK Gambling Industry by Key Sectors

+ Non-Remote Betting

| Non-Remote Betting GGY (£m) | ||||||||

|---|---|---|---|---|---|---|---|---|

| April 2008-March 2009 | April 2009-Mar 2010 | April 2010-March 2011 | April 2011-March 2012 | April 2012-March 2013 | April 2013-March 2014 | April 2014-March 2015 | April 2015-March 2016 | |

| Off course | 1,657.99 | 1,463.68 | 1,487.55 | 1,403.82 | 1,495.08 | 1,436.87 | 1,419.10 | 1,413.64 |

| On course | 27.76 | 29.18 | 26.42 | 29.28 | 24.18 | 25.85 | 23.23 | 21.68 |

| Pool | 146.50 | 135.56 | 136.08 | 137.99 | 131.64 | 143.07 | 142.96 | 127.50 |

| Total | 1,832.25 | 1,628.42 | 1,650.05 | 1,571.09 | 1,650.91 | 1,605.78 | 1,585.29 | 1,562.83 |

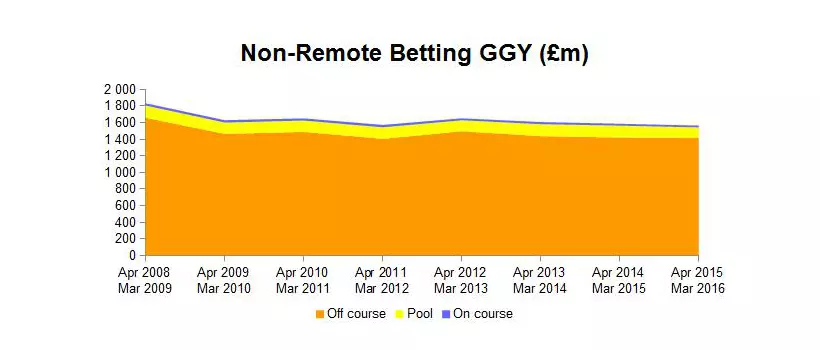

Table 2: Non-Remote Betting GGY (£m) – 2008-2016

Non-remote or retail betting has always been an important sector within the UK gambling industry. Local gambling customers have developed high preference for this type of service over the years. One of the main reasons for this is the fact that, as mentioned above, UK’s sports betting heritage spans centuries back.

As it can be seen in Table 2, the non-remote betting sector has increased over the years posting positive GGY growth every year with very few exceptions. Betting GGY dropped in the period between April 2009-March 2010 to £2.81 billion from £2.903 billion reported for the previous twelve months. A decrease was also posted for the period between April 2013-March 2014. GGY amounted to £3.175 billion during the reviewed twelve months.

Betting reached its highest in the reporting period April 2015-March 2016, when GGY of £3.306 billion was generated by the nation’s sports betting facilities.

Off-course betting has maintained a leadership position in the sector over the reported eight years. GGY from this type of operations has grown from £2.729 billion in the April 2008-March 2009 reporting period to £3.157 billion in the April 2015-March 2016 reporting period. There were only two years to have seen slight GGY drops. In the period between April 2009-March 2010, GGY slipped 3% year-on-year to £2.647 billion. A 1% drop was posted for the period April 2013-March 2014, when GGY of £3.006 billion was generated.

| Off-Course Betting GGY (£m) | ||||||||

|---|---|---|---|---|---|---|---|---|

| April 2008-March 2009 | April 2009-March 2010 | April 2010-March 2011 | April 2011-March 2012 | April 2012-March 2013 | April 2013-March 2014 | April 2014-March 2015 | April 2015-March 2016 | |

| Machines | 1,070.99 | 1,182.94 | 1,307.28 | 1,458.50 | 1,547.69 | 1,589.06 | 1,684.30 | 1,743.38 |

| Over the counter | 1,657.99 | 1,463.68 | 1,487.55 | 1,403.82 | 1,495.08 | 1,436.87 | 1,419.10 | 1,413.64 |

| Total | 2,728.98 | 2,646.62 | 2,794.82 | 2,862.32 | 3,042.77 | 3,005.93 | 3,103.40 | 3,157.02J36 |

Table 3: Off-Course Betting GGY (£m)

The off-course betting segment includes machine betting and over-the-counter services. As it could be seen from Table 3 over-the-counter betting was the higher grossing segment during the first three reviewed periods. However, it gave way to machine betting during the period April 2011-March 2012.

Here we consider it important to dwell a little more on machine betting as it has been a broadly discussed topic over the past several months. There are three categories of gaming machines that can be found at betting shops across the UK – B2, B3, and C devices. As the table above shows, B2 gaming machines or fixed-odds betting terminals (FOBTs) have dominated the machine betting sector within the industry. The average number of such devices between April 2008 and March 2016 was 33,610. Their number has increased to 34,684 in the April 2015-March 2016 reporting period from 31,439 in the April 2008-March 2009 reporting period.

FOBTs have been a hot topic over the past several years, and particularly over the past several months. These machines give customers the chance to bet up to £100 every 20 seconds, which, according to many, makes them highly addictive and therefore dangerous. Changes are expected to be implemented in the way UK’s B2 gaming machines market is regulated after MPs and influential members of the public urged for measures to be taken.

William Hill has been the operator to have run the most betting premises over the reported eight years. The company has managed the average number of 2,310 betting shops during the period in question. However, William Hill was replaced in November 2016 as the owner of the largest retail chain in the UK by newly formed Ladbrokes Coral. The latter currently runs more than 3,500 betting shops across the country.

On-course betting was a considerably less popular activity during the reported periods, particularly when compared to its off-course counterpart. On-course betting products have generated GGY of between £21.7 million and £29.3 million during the eight one-year periods between April 2008 and March 2016. Betting on horse and dog races have been the most highly preferred on-course activities, based on GGY figures.

Last but not least, pool betting should, too, be paid attention as a fairly popular activity to have engaged customers over the reported eight years. Betting on dogs, football, and horses, in that order, have been the activities to have generated the highest GGY. According to the figures posted by the Gambling Commission, pool betting reached its GGY highest in the period April 2008 to March 2009, when the amount of £146.5 million was generated. From that point on, GGY went up and down to have its lowest level in the period between April 2015-March 2016. It totalled £127.5 million during the twelve months in question.

+ Casino

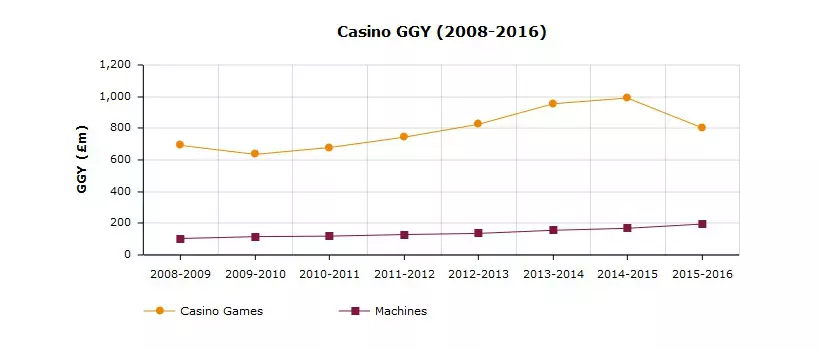

As shown in Table 4, casino (or table) games seem to have been the more widely preferred options in UK casinos, generating annual average GGY of £790.53 million for the period between April 2008-March 2016. Casino games generated their highest GGY of £991.16 million in the April 2014-March 2015 period. During the April 2008-March 2009 period, GGY of £692.28 million was reported, which indicates that interest in this type of land-based casino offering has increased relatively significantly over the years. Machine gambling has also seen a stable growth in the reported eight years.

| Casino GGY (£m) | ||||||||

|---|---|---|---|---|---|---|---|---|

| Apr 2008 Mar 2009 | Apr 2009 Mar 2010 | Apr 2010 Mar 2011 | Apr 2011 Mar 2012 | Apr 2012 Mar 2013 | Apr 2013 Mar 2014 | Apr 2014 Mar 2015 | Apr 2015 Mar 2016 | |

| Casino Games | 692.28 | 635.38 | 678.43 | 743.86 | 825.23 | 955.17 | 991.16 | 802.69 |

| Machines | 103.89 | 115.75 | 119 | 128.94 | 136.18 | 155.9 | 168.37 | 195.39 |

| Total | 796.17 | 751.13 | 797.43 | 872.8 | 961.41 | 1111.06 | 1159.53 | 998.08 |

Table 4: Casino GGY (£m)

Overall, the reporting periods April 2013-March 2014 and April 2014-March 2015 were the best for UK’s brick-and-mortar casino industry in terms of GGY generated. The amount of £1.1 billion was reported for the first period, followed by GGY of £1.2 billion for the second period.

The number of active land-based casinos has remained almost unchanged over the years. There were 143 operational premises as of 31 March 2009, compared to 148 such premises as of 31 March 2016.

Up until 2013, Genting UK, subsidiary of Malaysian gambling group Genting, was the largest operator of land-based casinos across the UK. However, in 2013, The Rank Group and Gala Coral finalized a deal, under which the former purchased the latter’s casino properties. From then on, The Rank Group has been operating the largest number of such facilities in the country. As of 31 March 2016, the gambling operator had 63 land-based casinos.

+ Remote

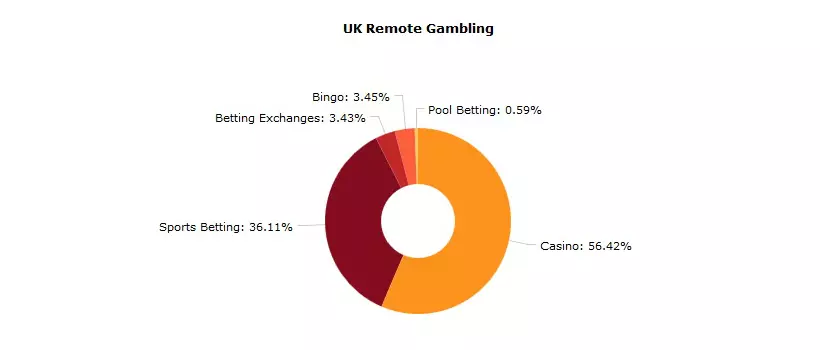

In terms of remote gambling (and here were refer mainly to online gambling), the UK is a good example of a trend that is yet to spread globally. The most recent financial report posted by the Gambling Commission showed that online gambling has become UK’s largest segment. The amount of £4.5 billion was generated in iGaming GGY during the twelve months ended 31 March 2016. A breakdown shows that online casino games represented the bulk of GGY reported for the period. This type of offering contributed £2.5 billion to the whole, or more than a half. A total of £1.8 billion came from online slots alone. Online sports betting generated £1.6 billion. Betting exchanges contributed £152 million. GGY from online bingo totalled £153 million. Pool betting accounted for a relatively small part of the whole. The amount of £26 million was generated from this type of online gambling options.

A quick look at Table 1 tells us that remote gambling has grown from a £816.86-million sector as of 31 March 2009 into a £4.5-billion one as of 31 March 2016. Overall, the sector has enjoyed a positive growth over the reported eight years, with the period April 2009-March 2010, when GGY of just £632.22 million was generated, being the only exception. And as it could be seen, after the Gambling (Licensing and Advertising) Act 2014 came into effect, remote gambling almost doubled to £2.238 billion during the twelve months ended 31 March 2015 from £1.135 billion during the prior-year period.

+ National Lottery

The National Lottery has remained a big contributor to the overall GGY generated over the years. The segment has never really stopped growing since 2009 when the Gambling Commission’s first report was published. As already mentioned, the National Lottery and sports betting were UK’s largest gambling sectors up until the April 2015-March 2016 period when online gambling encompassed the largest portion of the country’s gambling pie.

According to a recent report presented by Camelot Group, the National Lottery operator, there were more lottery millionaires in 2016 than any time before. As many as 347 players won jackpots of more than £1 million last year, compared to 341 lottery millionaires in 2015. It could be said that interest in this type of products has not decreased even after certain changes, ones that slimmed customers’ chances of a bigger win, have been introduced not long ago.

Conclusion

The UK gambling industry has been up to a continued growth over the past several years and the figures presented above are indication enough of that. Whether the upward trend will be maintained it only depends on how the industry will respond to the global trends, local regulatory changes, and customers’ demands.

One thing can be said with a degree of certainty – with looming tax and other regulatory amendments, the UK gambling landscape is set to change this year or in the next few years, just as it did in 2014 when the Gambling (Licensing and Advertising) Act 2014 came into effect.

- Author